Top US Dividend Stocks To Consider In February 2025

As of February 2025, the U.S. stock market has been experiencing a downturn, with major indexes like the S&P 500 and Dow Jones Industrial Average posting weekly losses following disappointing jobs and consumer sentiment reports. In such volatile times, dividend stocks often appeal to investors seeking stability and income through regular payouts, making them a potential consideration for those navigating uncertain market conditions.

Top 10 Dividend Stocks In The United States

| Name | Dividend Yield | Dividend Rating |

| Columbia Banking System (NasdaqGS:COLB) | 5.18% | ★★★★★★ |

| Interpublic Group of Companies (NYSE:IPG) | 4.80% | ★★★★★★ |

| Peoples Bancorp (NasdaqGS:PEBO) | 4.84% | ★★★★★★ |

| FMC (NYSE:FMC) | 6.72% | ★★★★★★ |

| Dillard's (NYSE:DDS) | 5.49% | ★★★★★★ |

| Southside Bancshares (NYSE:SBSI) | 4.54% | ★★★★★★ |

| Regions Financial (NYSE:RF) | 5.83% | ★★★★★★ |

| First Interstate BancSystem (NasdaqGS:FIBK) | 5.72% | ★★★★★★ |

| Citizens & Northern (NasdaqCM:CZNC) | 5.19% | ★★★★★★ |

| Virtus Investment Partners (NYSE:VRTS) | 4.76% | ★★★★★★ |

Click here to see the full list of 135 stocks from our Top US Dividend Stocks screener.

Let's dive into some prime choices out of the screener.

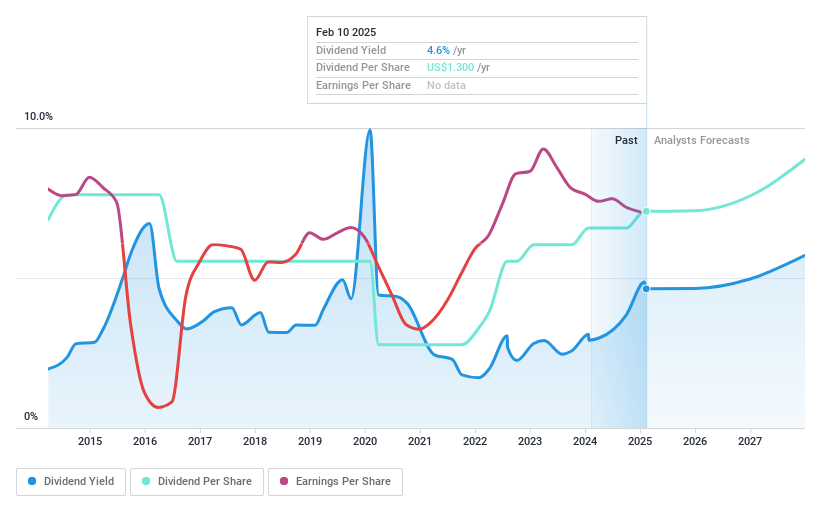

Brookline Bancorp (NasdaqGS:BRKL)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Brookline Bancorp, Inc. is a bank holding company for Brookline Bank, offering commercial, business, and retail banking services to corporate, municipal, and retail customers in the United States with a market cap of approximately $1.12 billion.

Operations: Brookline Bancorp, Inc. generates revenue primarily through its banking business segment, which accounted for $333.56 million.

Dividend Yield: 4.3%

Brookline Bancorp offers a reliable dividend yield of 4.31%, though slightly below the top tier in the US market. Its dividends have been stable and growing over the past decade, supported by a reasonable payout ratio currently at 69.9%. Earnings are forecast to grow significantly, suggesting potential sustainability of dividends. Recent earnings showed decreased net income, but Brookline is set to merge with Berkshire Hills Bancorp in an all-stock transaction valued at $1.1 billion, potentially enhancing future financial stability and growth opportunities for shareholders.

- Get an in-depth perspective on Brookline Bancorp's performance by reading our dividend report here.

- Our comprehensive valuation report raises the possibility that Brookline Bancorp is priced lower than what may be justified by its financials.

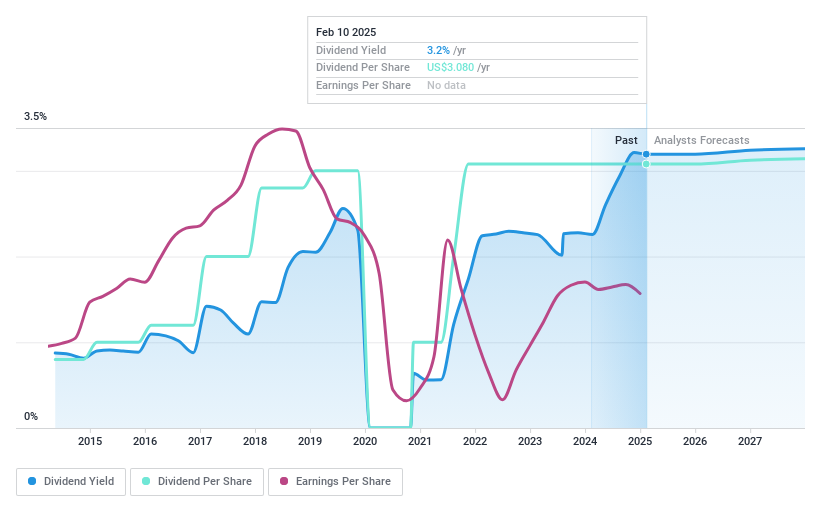

Lear (NYSE:LEA)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Lear Corporation operates in the automotive industry, providing seating and electrical distribution systems for original equipment manufacturers across multiple continents, with a market cap of approximately $5.22 billion.

Operations: Lear Corporation's revenue is derived from its Seating segment, which generates $17.22 billion, and its e-Systems segment, contributing $6.08 billion.

Dividend Yield: 3.2%

Lear Corporation's dividend payments are well covered by earnings and cash flows, with a payout ratio of 34.4% and cash payout ratio of 37.3%. Despite this coverage, dividends have been volatile over the past decade, lacking reliability. Trading significantly below estimated fair value, Lear offers a relatively low dividend yield of 3.2%. Recent earnings showed decreased net income year-over-year, while new product innovations like ComfortMax Seat may support future growth and operational efficiency improvements.

- Delve into the full analysis dividend report here for a deeper understanding of Lear.

- Our valuation report unveils the possibility Lear's shares may be trading at a discount.

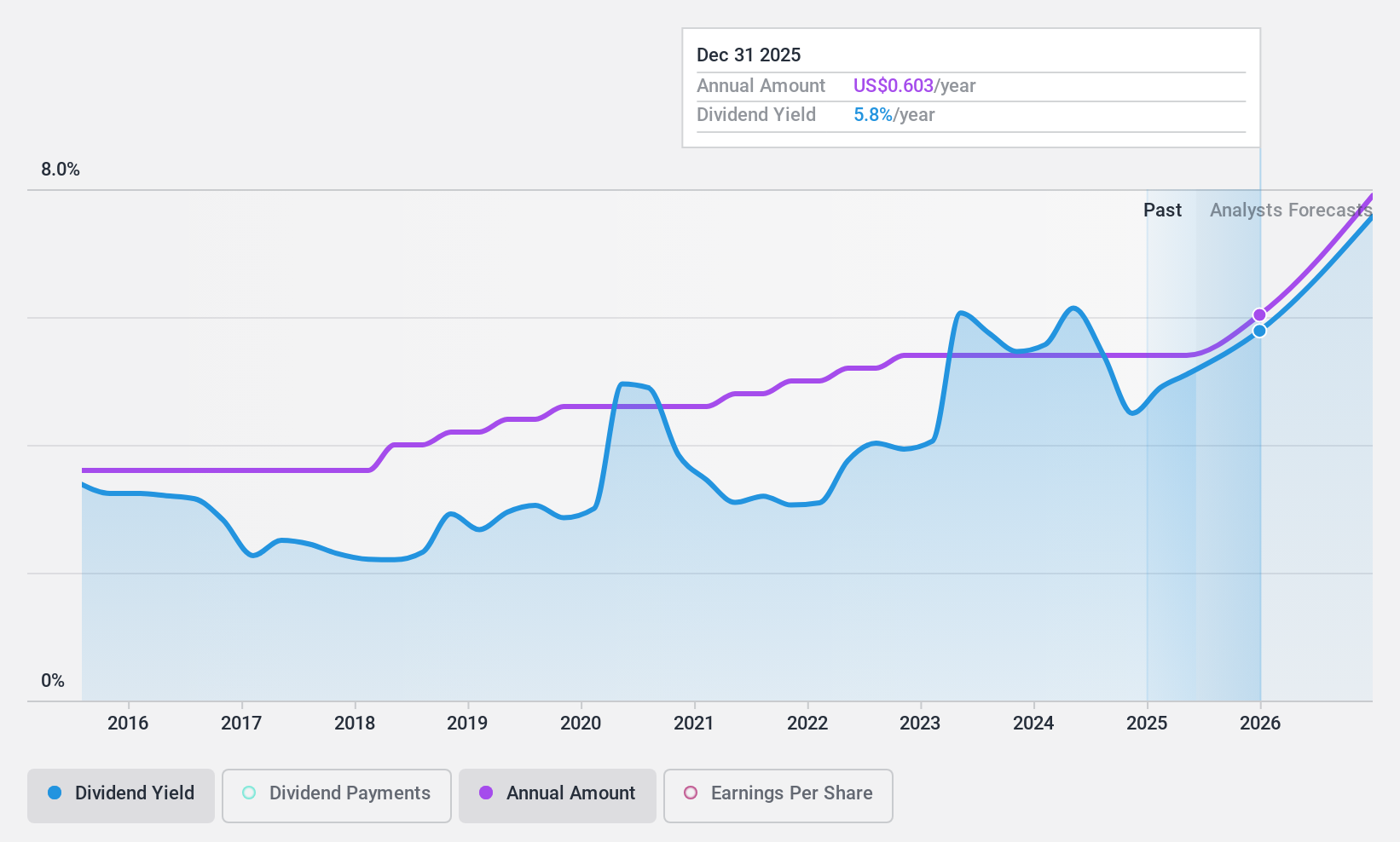

Murphy Oil (NYSE:MUR)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Murphy Oil Corporation, along with its subsidiaries, is an oil and gas exploration and production company operating in the United States, Canada, and internationally, with a market cap of approximately $3.91 billion.

Operations: Murphy Oil Corporation's revenue segments include Exploration and Production in the United States at $2.51 billion and Canada at $509.70 million.

Dividend Yield: 4.8%

Murphy Oil's dividends are well covered by earnings and cash flows, with a payout ratio of 44.8% and a cash payout ratio of 23.1%. Despite past volatility in dividend payments, the company has recently increased its quarterly dividend to US$0.325 per share. Trading below estimated fair value, Murphy Oil offers a competitive yield in the top quartile of US dividend payers at 4.85%. Recent earnings showed decreased net income year-over-year amidst ongoing production guidance updates for 2025.

- Take a closer look at Murphy Oil's potential here in our dividend report.

- Insights from our recent valuation report point to the potential undervaluation of Murphy Oil shares in the market.

Seize The Opportunity

- Embark on your investment journey to our 135 Top US Dividend Stocks selection here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10