ASX Stocks Estimated To Be Up To 43.4% Below Intrinsic Value

The Australian stock market has shown mixed performance recently, with the ASX200 closing slightly down amid geopolitical developments affecting global trade. While sectors like IT and Materials have seen gains, others such as Real Estate and Energy have faced declines, highlighting the importance of identifying stocks that may be undervalued in these fluctuating conditions. In this context, discerning investors often look for stocks trading below their intrinsic value, offering potential opportunities for growth despite broader market uncertainties.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| SKS Technologies Group (ASX:SKS) | A$2.14 | A$3.82 | 44% |

| Mader Group (ASX:MAD) | A$6.21 | A$11.90 | 47.8% |

| Pureprofile (ASX:PPL) | A$0.048 | A$0.092 | 47.8% |

| Atlas Arteria (ASX:ALX) | A$4.95 | A$9.56 | 48.2% |

| Champion Iron (ASX:CIA) | A$5.355 | A$9.60 | 44.2% |

| MLG Oz (ASX:MLG) | A$0.60 | A$1.17 | 48.6% |

| SciDev (ASX:SDV) | A$0.46 | A$0.87 | 47.3% |

| Charter Hall Group (ASX:CHC) | A$15.46 | A$28.75 | 46.2% |

| ReadyTech Holdings (ASX:RDY) | A$3.21 | A$6.16 | 47.9% |

| Syrah Resources (ASX:SYR) | A$0.235 | A$0.42 | 44.2% |

Click here to see the full list of 43 stocks from our Undervalued ASX Stocks Based On Cash Flows screener.

Here we highlight a subset of our preferred stocks from the screener.

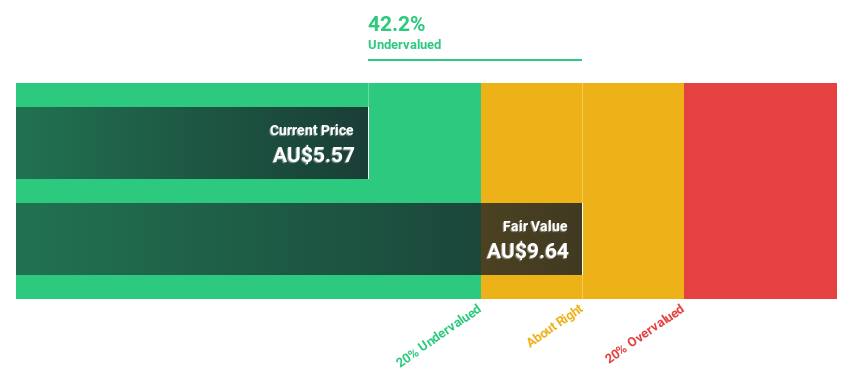

Data#3 (ASX:DTL)

Overview: Data#3 Limited provides information technology solutions and services across Australia, Fiji, and the Pacific Islands, with a market cap of A$1.07 billion.

Operations: The company generates revenue of A$805.75 million from its role as a value-added IT reseller and IT solutions provider in the specified regions.

Estimated Discount To Fair Value: 43.4%

Data#3 is trading at A$6.93, significantly below its estimated fair value of A$12.25, indicating it may be undervalued based on cash flows. Despite a dividend yield of 3.72% not being well covered by earnings or free cash flows, the company has shown strong earnings growth of 17% over the past year and is expected to maintain robust revenue growth at 23.8% annually, outpacing the broader Australian market's growth rate.

- Upon reviewing our latest growth report, Data#3's projected financial performance appears quite optimistic.

- Delve into the full analysis health report here for a deeper understanding of Data#3.

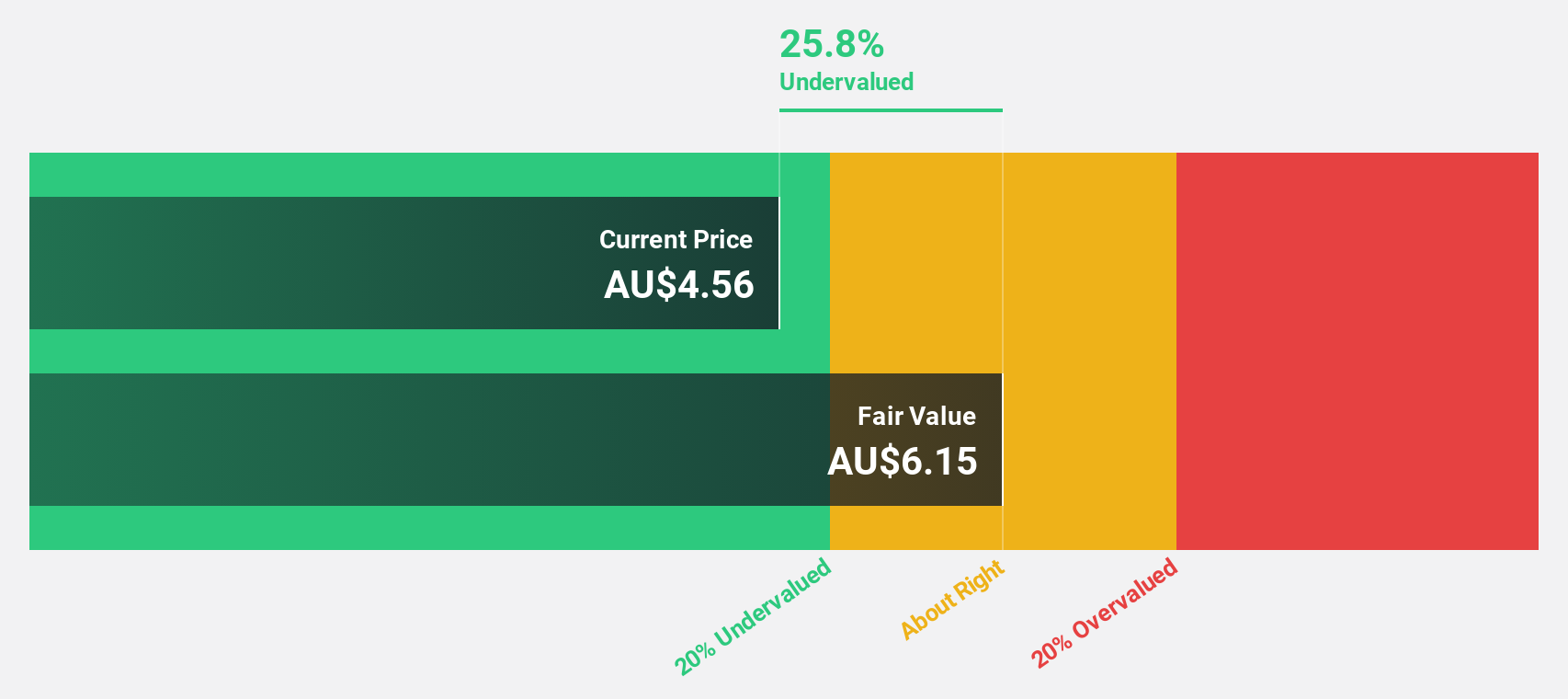

Genesis Minerals (ASX:GMD)

Overview: Genesis Minerals Limited is involved in the exploration, production, and development of gold deposits in Western Australia with a market cap of A$3.60 billion.

Operations: The company generates revenue of A$438.59 million from its activities in mineral production, exploration, and development.

Estimated Discount To Fair Value: 33.1%

Genesis Minerals is trading at A$3.19, below its estimated fair value of A$4.77, suggesting undervaluation based on cash flows. The company recently became profitable and is projected to achieve substantial earnings growth of 25.6% annually over the next three years, surpassing the Australian market's average growth rate. However, its forecasted Return on Equity remains relatively low at 16.5%. Upcoming earnings results are anticipated in December 2024 following recent investor presentations in Sydney and Melbourne.

- Our expertly prepared growth report on Genesis Minerals implies its future financial outlook may be stronger than recent results.

- Dive into the specifics of Genesis Minerals here with our thorough financial health report.

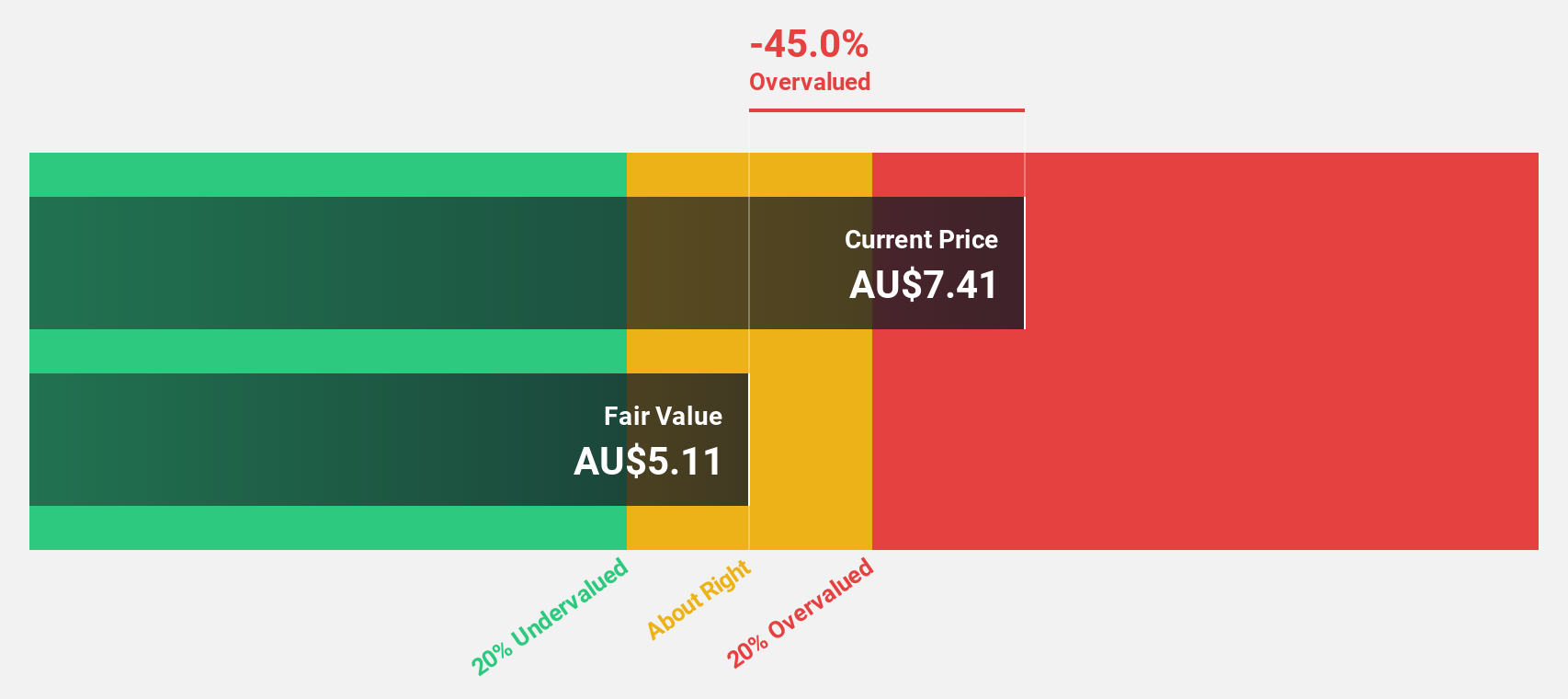

Whitehaven Coal (ASX:WHC)

Overview: Whitehaven Coal Limited develops and operates coal mines in New South Wales and Queensland, with a market cap of A$5.15 billion.

Operations: The company generates revenue primarily from its operations in New South Wales, contributing A$2.85 billion, and Queensland, which adds A$869 million.

Estimated Discount To Fair Value: 39.3%

Whitehaven Coal, priced at A$6.16, appears undervalued with a fair value estimate of A$10.14 and trades 39.3% below this estimate. Despite lower profit margins compared to last year, earnings are forecast to grow significantly at 21.54% annually over the next three years, outpacing the Australian market's growth rate of 12.5%. However, its Return on Equity is expected to be modest at 11.1%, and its dividend coverage is weak due to large one-off items affecting results.

- According our earnings growth report, there's an indication that Whitehaven Coal might be ready to expand.

- Navigate through the intricacies of Whitehaven Coal with our comprehensive financial health report here.

Taking Advantage

- Click here to access our complete index of 43 Undervalued ASX Stocks Based On Cash Flows.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Whitehaven Coal might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10